Frothy stockmarkets

泡沫股市

Fit to burst

一触即溃

How to hedge your portfolio during a bubble On February 8th sports fans watch-sports fans watching the Super Bowl, an American-foot-ballgame, were treated to an ad for Claude, an artificial-intelligence chatbot. That might have given investors with long memories an unsettling sense of deja vu. The Super Bowl of 2000 passed into market folklore as having epitomised internet-stock mania: no fewer than 17 "dotcom" firms paid millions of dollars each for 30-second advertising slots. Weeks later share prices fell into a brutal bear market.2月8日,观看美国职业橄榄球总决赛“超级碗”的体育迷们欣赏到了一则人工智能聊天机器人Claude的广告。这或许会让记忆犹新的投资者产生一种不安的似曾相识感。2000年的超级碗已成为市场传说中互联网股票狂热的缩影:当时有超过17家"互联网公司"各自斥资数百万美元购买30秒的广告时段。几周后,股价便陷入惨烈的熊市。Folklore /ˈfəʊklɔː(r)/ n. 民俗学;民间传说Epitomised /ɪˈpɪtəmaɪzd/ v. 成为…的缩影;代表(epitomise的过去式/过去分词)Slots /slɒts/ n. 位置;狭缝;时间段(slot的复数形式)Brutal /ˈbruːtl/ adj. 残忍的;野蛮的;直截了当的Back in the present, investors' confidence in today's emerging technology-AI-has already begun to wobble, just as companies prepare to spend jaw-dropping amounts of money to develop it. In recent weeks Alphabet, Amazon, Meta and Microsoft have said they will spend a combined $660bn on AI in the coming year. Investors who a year ago might have cheered such plans are getting cold feet. Each firm's stock price has fallen since its announcement, though Meta's shot up at first. Microsoft's is down by 16%. 回到当下,就在众多公司准备投入惊人资金发展人工智能(AI)之际,投资者对这项新兴技术的信心却已开始动摇。最近几周,Alphabet、亚马逊、Meta和微软相继宣布,未来一年将在AI领域合计投入6600亿美元。那些一年前或许还会为这类计划欢呼的投资者现在却打起了退堂鼓。自各家公司公布相关计划以来,尽管Meta的股价起初曾一度飙升,但随后每家公司的股价均出现下跌。其中,微软的股价已下跌16%。Wobble /ˈwɒbl/ v. 摇晃;颤抖;犹豫

Jaw-dropping /ˈdʒɔː drɒpɪŋ/ adj. 令人瞠目结舌的;非常惊人的

Shot up /ʃɒt ʌp/ v. 飞速上升;猛增(shoot up的过去式/过去分词)

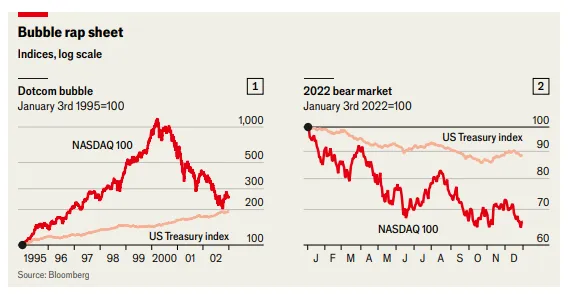

It is no wonder that markets feel jittery. Everyone knows that shares are expensive-especially in America, but increasingly elsewhere, too. When stock prices are high relative to underlying earnings, expected returns are low and shareholders have more to lose from a crash. The trouble is knowing which other assets might offer refuge. The price of gold, investors' time-honoured safe haven, has swung wildly of late. One-time fans of bitcoin, a digital pretender, are losing the faith (see Button-wood). Just as investors are searching for ways to hedge their equity risk, hedging opportunities seem few and far between.难怪市场会感到不安。谁都知道股票很贵——尤其是在美国,但其他地方也越来越如此。当股价相对于基础收益较高时,预期回报率就会降低,股东在股市崩盘时可能蒙受的损失就更大。问题在于,不知道该选择哪些其他资产来避险。投资者传统的避险资产黄金的价格最近剧烈波动。一度受到追捧的数字货币比特币也正失去拥趸(参见梧桐专栏)。就在投资者想方设法对冲股票风险之时,对冲的机会似乎少之又少。Jittery /ˈdʒɪtəri/ adj. 紧张不安的;战战兢兢的Haven /ˈheɪvn/ n. 避难所;安息所Pretender /prɪˈtendə(r)/ n. 伪装者;觊觎者The most obvious way to protect yourself from a stockmarket crash is to sell your stocks. Yet for most professional investors this is not an option. Some swashbuckling hedge funds can allocate their portfolios however they please, but most money managers face strict limits. When someone entrusts their capital to an equity fund, for example, they expect it to be invested in equities. Often, the portfolio manager's mandate will prevent them from sitting on a pile of cash; if not, doing so would still invite angry calls from clients, followed by withdrawals. They can keep cash in their own bank accounts, after all, without paying the manager's fees.保护自己免受股市崩盘影响的最明显方法是卖出股票。然而,对于大多数专业投资者来说,这并不是一个选择。一些激进的对冲基金可以随心所欲地配置投资组合,但大多数基金经理面临着严格的限制。例如,当某人将资金委托给股票基金时,他们期望这些资金被投资于股票。通常,基金经理的授权会阻止他们持有大量现金;即使没有这样的限制,这样做也会招致客户的愤怒电话,随后是赎回。毕竟,客户可以把现金存在自己的银行账户里,无需支付基金经理的费用。生词Swashbuckling /ˈswɒʃbʌklɪŋ/ adj. 英雄了得的;神勇张狂的;(商业上)敢作敢为的Portfolios /pɔːrtˈfoʊlioʊz/ n. 投资组合;文件夹;(政府部门的)职责(portfolio的复数形式)Mandate /ˈmændeɪt/ n. 授权;委任;指令Withdrawals /wɪðˈdrɔːəlz/ n. 提款;取回;撤退(withdrawal的复数形式)Individuals have no such restrictions, but selling up because stocks look pricey can still be a bad strategy. During the dotcom bubble, the valuation of the tech-heavy NASDAQ index relative to expected underlying earnings rose to multiples of its current level. In the five years to its peak in March 2000 the index suffered corrections of 10% or more on at least a dozen occasions. Any of these might have prompted the nervous to cut their losses. Over the same period, however, it ultimately rose nearly 12-fold. Even at the bottom of the subsequent plunge, investors who had simply bought at the start of 1995 and held on would have doubled their money.个人投资者虽无此限制,但仅因股价偏高就清仓离场仍可能失策。在互联网泡沫时期,以科技股为主的纳斯达克指数相对于预期基础收益的估值曾攀升至当前水平的数倍之多。在截至2000年3月峰值的五年间,该指数经历了至少12次10%或以上的回调。任何一次回调都可能促使 焦虑的投资者止损离场。然而,在同一时期,该指数最终上涨了近12倍。即便在随后的暴跌谷底,那些在1995年初买入并一直持有的投资者,其资金也已翻倍。生词Dotcom /ˌdɒtˈkɒm/ n. 网络公司;互联网企业Plunge /plʌndʒ/ v. 暴跌;骤降;纵身一跳A good strategy for hedging stock market risk is one that does not suppress returns too much on the way up, then cushions losses on the way down. Sifting through the wreckage of the dotcom crash is a helpful way to think about how the various candidates might perform today. Broadly, they fit into three categories: the classic split between stocks and bonds; exotic strategies involving derivatives; and the use of alternative diversifiers.对冲股市风险的好策略应当既不过分压制上涨期的收益,又能在下跌时缓冲损失。梳理互联网泡沫破裂时期的残骸,有助于思考当下各种可能的策略会如何表现。大致可分为三类:经典的股票与债券配置、涉及衍生品的另类策略,以及使用替代性分散投资工具。生词Cushions /ˈkʊʃnz/ n. 缓冲物;垫子;(金融)储备金(cushion的复数形式)Sifting /ˈsɪftɪŋ/ v. 筛选;过滤;仔细检查(sift的现在分词)Wreckage /ˈrekɪdʒ/ n. 残骸;碎片;(计划或组织的)失败Exotic /ɪɡˈzɒtɪk/ adj. 异国的;外来的;(金融)奇异的Diversifiers /daɪˈvɜːrsɪfaɪərz/ n. 多样化投资工具;分散风险的资产(diversifier的复数形式)For asset allocators with the freedom to do so, buffering stocks with bonds would have worked well during the late 1990s. The borrowing costs of rich-world governments were falling as the high inflation of the 1980s faded into memory, granting windfall gains to bond holders (since prices move inversely to yields). From early 1995 to the NASDAQ's March 2000 peak, Bloomberg's index tracking the total returns from a basket of American Treasuries rose by nearly 50%. As share prices plummeted, central bankers slashed interest rates and bondholders benefited from falling yields again. As the NASDAQ fell from peak to trough, the Bloomberg Treasury index rose by another 30% (see chart 1).对于拥有配置自由的投资组合经理来说,上世纪90年代末,用债券来缓冲股票风险本可以非常有效。随着80年代的高通胀逐渐淡出记忆,富裕国家政府的借贷成本不断下降,债券持有者获得了意外之财(因为价格与收益率走势相反)。从1995年初到2000年3月纳斯达克指数见顶期间,彭博一篮子美国国债总回报指数上涨了近50%。随着股价暴跌,央行大幅降息,债券持有人再次从收益率下降中受益。在纳斯达克指数从峰值跌至谷底的过程中,彭博国债指数又上涨了30%(见图1)。Buffering /ˈbʌfərɪŋ/ n. 缓冲;减震(buffix的现在分词/动名词形式)Plummeted /ˈplʌmɪtɪd/ v. 暴跌;垂直落下(plummet的过去式/过去分词)Slashed /slæʃt/ v. 大幅削减;劈砍(slash的过去式/过去分词)It is not clear, however, that government bonds are still as useful for hedging equity risk today. During the last prolonged bear market, in 2022, both asset classes suffered as inflation rose sharply and interest rates followed (see chart 2). Ask investors today what might end stock-markets' bull run, and resurgent inflation-and the hawkish response it would require from central bankers-will top plenty of lists. That would mean share and bond prices falling in tandem once more.然而,目前尚不清楚政府债券是否仍像过去那样能有效对冲股票风险。在最近一次2022年的长期熊市中,随着通胀大幅上升和利率随之走高,这两类资产都遭受了损失(见图2)。若问当今的投资者什么可能终结股市的牛市,通胀再度抬头——以及它将引发的央行鹰派反应——会在许多人的清单上位居前列。那将意味着股票和债券价格再次同步下跌。

生词

Suffered /ˈsʌfəd/ v. 遭受;受苦;经历(痛苦、损害等)Resurgent /rɪˈsɜːrdʒənt/ adj. 复苏的;再度崛起的Hawkish /ˈhɔːkɪʃ/ adj. 鹰派的;主张强硬政策的Tandem /ˈtændəm/ n. 串联;协同;双人自行车Feeling liberated

Others will recall the short-lived panic that followed the unveiling of President Donald Trump's "Liberation Day" tariffs last April. Then, for a brief spell, Treasuries and stocks also dropped together as investors worried that the White House's erratic policy making would endanger the bonds' status as a haven asset for international investors. It is easy to imagine the next leg down in share prices being triggered by similar concerns, or by questions over the sustainability of rich-world governments' vast borrowing. In either case, stocks and bonds would both be in the firing line.

另一些人则会回想起去年四月特朗普总统的“解放日”关税政策公布后引发的短暂恐慌。当时,由于投资者担心白宫反复无常的政策制定会危及美国国债作为国际投资者避险资产的地位,美国国债和股票曾一度同步下跌。不难想象,下一轮股价下跌同样可能由类似的担忧引发,或者源于对富裕国家政府巨额借贷可持续性的质疑。无论哪种情况,股票和债券都将同时面临冲击。

生词

Unveiling /ʌnˈveɪlɪŋ/ n. 揭幕;发布;正式公开(unveil的现在分词/动名词形式)

Erratic /ɪˈrætɪk/ adj. 古怪的;反复无常的;不稳定的

A second category of hedging strategies involves derivative contracts called options. These have long been used by hedge-fund managers and other professional investors, but are increasingly sold by retail brokers, too. "Overlaying" a stock portfolio with options allows an investor to harvest most of the profits when share prices are rising, then to restrict their losses once the cycle turns.第二类对冲策略涉及被称为期权的衍生品合约。这些工具长期以来一直为对冲基金经理和其他专业投资者所使用,但现在也越来越多地通过零售经纪商销售给普通投资者。通过用期权“叠加”股票投资组合,投资者可以在股价上涨时获取大部分利润,并在市场周期逆转时限制损失。

A "put" option on a stock, for example, confers the right but not the obligation to sell the stock at a pre-agreed "strike" price on some specified future date. If you also own the underlying stock, the effect is to cut off your potential losses beyond a certain point. Set the strike at 90% of the current price, say, and the option to sell at that strike means you cannot lose more than 10% of your initial holding. A put option on the S&P 500 share index that limits losses to 10% over the coming year currently costs 3.6% of the underlying amount to be protected. In other words, an investor who agrees to give up 3.6 percentage points of their returns can be protected from a crash.以股票的“看跌”期权为例,它赋予持有者在未来某个指定日期以预先约定的“行权价”卖出该股票的权利,而非义务。如果你同时也持有该标的股票,其效果就是将你的潜在损失限制在某一水平以下。比如,将行权价设定为当前价格的90%,那么以此价格卖出股票的期权就意味着你的初始持仓损失不会超过10%。目前,一份将未来一年损失限制在10%以内的标普500股指看跌期权,其成本相当于所保护标的金额的3.6%。换句话说,愿意牺牲3.6个百分点收益的投资者,便可获得免受崩盘冲击的保护。Confers /kənˈfɜːrz/ v. 授予;给予(权利、荣誉等);商谈Obligation /ˌɒblɪˈɡeɪʃn/ n. 义务;责任;契约The trouble is that the performance of such hedges depends heavily on the choice of strike price and expiration date. Analysts at Goldman Sachs, a bank, compared how two strategies using put options on the S&P 500 would have performed from 1996 to 2002. One involved buying a series of one-year options, each limiting losses to 10%; the other, a series of one-month options limiting losses to 4%. Though both would have offered protection as the dotcom bubble burst, the costs of repeated option purchases would have snowballed. Overlaying a stock portfolio with the one-year options would have resulted in roughly the same annualised return as unhedged stocks (albeit with less volatility). Overlaying it with one-month options would have generated a substantially worse return, despite the crash.问题在于,此类对冲策略的效果高度依赖于行权价和到期日的选择。高盛银行分析师对比了1996年至2002年间两种标普500指数看跌期权策略的表现:第一种策略是逐年买入一年期期权,将年度损失上限设定为10%;第二种策略则是逐月买入一月期期权,将月度损失上限设定为4%。虽然这两种策略都能在互联网泡沫破裂时提供保护,但反复购买期权的成本会如滚雪球般持续累积。若将一年期期权叠加于股票组合,其年化收益率与未对冲股票基本持平(尽管波动性较低),而采用一月期期权策略的投资组合即使经历市场崩盘,其收益率仍显著逊色。Some of the most effective strategies the Goldman analysts found fell into the third category: combinations of stocks and non-bond diversifiers. In fact, the best diversifiers were mostly filtered baskets of stocks, such as the S&P 500 "low volatility" subindex, which includes the 100 least volatile stocks in the main index. A 50/50 split between this and the S&P 500 would, from 1996 to 2002, have generated nearly twice the annualised excess returns (overcash) of the S&P 500 index alone. So would a similar split with the S&P 500 "dividend aristocrats" index, which includes only companies that have increased their dividends every year for the past 25. Diversifying into "quality" stocks (with high returns on equity, stable earnings and low net debt) would have brought similar returns.高盛分析师发现,部分最有效的策略属于第三类:股票与非债券型分散工具的复合配置。事实上,最佳分散工具多为经过筛选的股票篮子,例如标普500"低波动率"子指数——该指数由主指数中波动率最低的100只成分股构成。若将此类资产与标普500指数进行五五开配置,1996年至2002年间产生的年化超额收益(相对于现金)近乎纯标普500指数的两倍。采用相同比例配置标普500"股息贵族"指数(仅纳入连续25年提高股息的企业)也能获得类似回报。而将"优质股"(净资产收益率高、盈利稳定、净负债率低)纳入投资组合,同样能带来相近的收益表现。Subindex /ˈsʌbɪndeks/ n. 分指数;子指数;下标Split /splɪt/ v./n. 分裂;拆分;(股票)拆股Dividend /ˈdɪvɪdend/ n. 红利;股息;被除数Aristocrat /ˈærɪstəkræt/ n. 贵族;(同类中)最优秀者Today, the idea that the best way to hedge equity risk is with equities feels unsatisfying. Considering the alternatives, though, it might just be the best shareholders can do.如今,用股票对冲股票风险的说法难免令人心生疑虑。但权衡各种替代方案后,这或许已是投资者能做出的最优选择。文:《The Economist》

译:Nancy